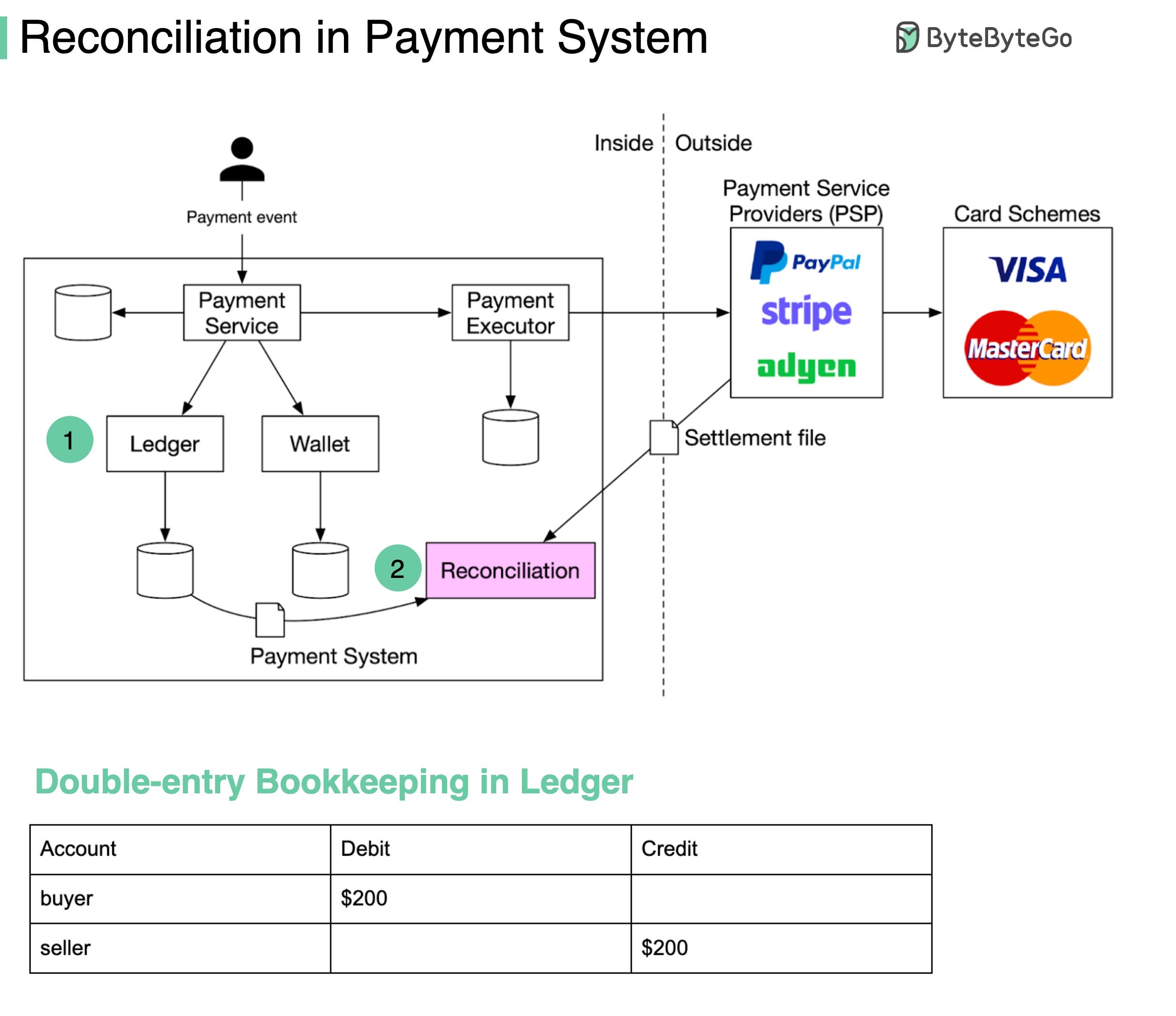

Painful payment reconciliation

My previous post about painful payment reconciliation sparked lots of interesting discussions. One of the readers shared more problems we may face when working with intermediary payment processors in the trenches and a potential solution:

1. Foreign Currency Problem: When you operate a store globally, you will come across this problem quite frequently. To go back to the example from Paypal - if the transaction happens in a currency different from the standard currency of Paypal, this will create another layer, where the transaction is first received in that currency and exchanged to whatever currency your Paypal is using. There needs to be a reliable way to reconcile that currency exchange transaction. It certainly does not help that every payment provider handles this differently.

2. Payment providers are only that - intermediaries. Each purchase does not trigger two events for a company, but actually at least 4. The purchase via Paypal (where both the time and the currency dimension can come into play) trigger the debit/credit pair for the transaction and then, usually a few days later, another pair when the money is transferred from Paypal to a bank account (where there might be yet another FX discrepancy to reconcile if, for example, the initial purchase was in JPY, Paypal is set up in USD and your bank account is in EUR). There needs to be a way to reconcile all of these.

3. Some problems also pop up on the buyer side that is very platform-specific. One example is shadow transaction from Paypal: if you buy two items on Paypal with 1 week of time between the two transactions, Paypal will first debit money from your bank account for transaction A. If at the time of transaction B, transaction A has not gone through completely or is canceled, there might be a world where Paypal will use the money from transaction A to partially pay for transaction B, which leads to only a partial amount of transaction B being withdrawn from the bank account.

In practice, this usually looks something like this:

1) Your shop assigns an order number to the purchase

2) The order number is carried over to the payment provider

3) The payment provider creates another internal ID, which is carried over across transactions within the system

4) The payment ID is used when you get the payout on your bank account (or the payment provider bundles individual payments, which can be reconciled within the payment provider system)

5) Ideally, your payment provider and your shop have an integration/API with the tool you use to (hopefully automatically) create invoices. This usually carries over the order id from the shop (closing the loop) and sometimes even the payment id to match it with the invoice id, which you then can use to reconcile it with your accounts receivable/payable. :)

Credit: A knowledgeable reader who prefers to stay private. Thank you!

If you enjoyed this post, you might like our system design interview books as well.

SDI-vol1: https://amzn.to/3tK0qQn

SDI-vol2: https://amzn.to/37ZisW9

thanks to that knowledgeable anonymous reader